The recent visit to Canada by the Japanese Prime Minister sparked the latest round of debate about the prospects for increasing Canadian LNG production and export.

According to LNG champions, “Canada definitely has a business case for LNG.” The basic premise is that increasing LNG exports from Canada can help wean Japan off Russian gas and cut greenhouse (GHG) emissions by replacing coal. A win for the energy security of an ally, and a win for the climate.

The story goes on to say that Japan might even consider using Article 6 of the Paris Agreement to transfer credits for their GHG emission reductions to Canada, which could count towards achieving Canada’s 2030 target and offset the additional GHG emissions from producing and liquefying more gas. Win-win-win!

It sure sounds like a great story, but does it live up to the hype?

For policymakers, there are two, interrelated considerations at the intersection of the business case and the public interest.

The first is whether direct (e.g. tax breaks, grants) or indirect (e.g. helping foot the bill for new electricity transmission to electrify operations) public subsidies are warranted. The sweet spot is when the economic benefits are significant and fairly certain, and providing subsidies tips the scales on the business case for investment.

The second relates to climate change and the growing momentum towards clean (i.e. zero carbon) energy. What are the domestic GHG emission implications? What about global GHG emissions? And how do these considerations impact competitiveness and the risk of stranded assets?

Let’s take a closer look at where things are tracking in Japan, and how this ought to inform the debate about LNG exports from Canada.

According to the IEA’s 2022 World Energy Outlook, in a business-as-usual scenario (which they call Stated Policies, or STEPS), Japan’s demand for natural gas is projected to decrease by 39 million cubic metres (bcm)—or 38%— by 2030, relative to 2021, as the 2021 Strategic Energy Plan is implemented. This plan was formulated along two key themes: (1) achieving carbon neutrality by 2050 and the greenhouse gas emission reduction target, and (2) ensuring stable energy supply and reducing its costs while taking action against climate change. (IEA, 2022)

If Japan follows through on announced policies (the IEA’s Announced Policies Scenario, or APS)—which include the Green Transformation (GX) plan, which the Japanese Cabinet has subsequently approved—the drop in gas demand to 2030 is even more pronounced, falling by 57 bcm, or 58%. And it doesn’t stop there. By 2050 gas demand is projected to be just 17 bcm, an 83% drop from 2021. It’s also critical to note that as demand gas drops, so too does demand for coal—falling by 40 (STEPS) to 46 million (APS) tonnes per year by 2030.

As we have witnessed in the EU’s response to the energy crisis resulting from the Russian invasion of Ukraine, energy security and climate security are no longer at odds. As the IEA put it, “this is a crisis where energy transitions are the solution, rather than the problem.” (IEA, 2022)

This is similarly evident in Japan’s plans for “working to reduce its energy security risks while pushing forward with its climate agenda through measures to decrease exposure to imported fossil fuels, increase its share of nuclear and renewables, and improve energy efficiency.” (IEA, 2022)

But if both gas and coal demand is falling, then the specific question at hand doesn’t have a climate dimension, it’s really just about replacing Russian gas with Canadian gas. And so we must ask ourselves: if the role of Canadian gas is simply to replace Russian gas, how will it fare as Japanese gas demand falls?

Japan really doesn’t import much Russian gas, so it won’t be long before there are more non-Russian suppliers than there is demand. Will Canadian gas still be able to compete with other suppliers in this scenario, or will Canadian LNG terminals end up as stranded assets?

Source: IEA

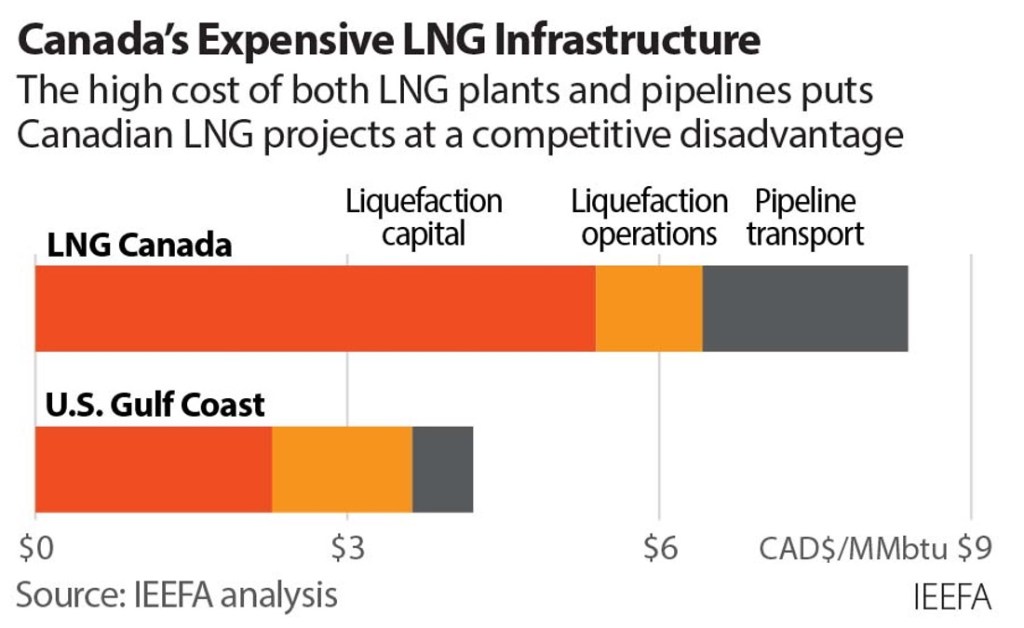

According to a recent analysis exploring the relative cost of Canadian versus American LNG, competing on cost will be challenging:

Source: IEEFA

This raises questions about whether there’s enough certainty of success to justify public subsidies. It took several billion in subsidies to secure a final investment decision for Phase 1 of the LNG Canada project, but that was when the outlook for gas was much rosier than it is today. Back then the IEA was still touting the “golden age of gas.” Now, the IEA has declared “The golden age of gas is approaching the end.” (IEA, 2022)

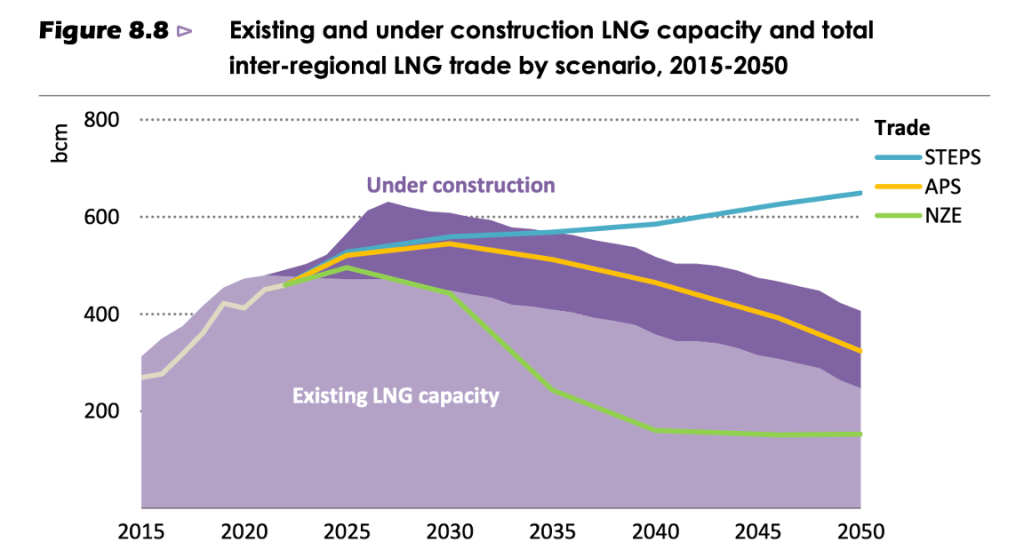

How fast is it approaching that end? For LNG capacity, it appears we’re already there. According to the IEA, if governments follow through on policies they’ve announced (APS)—as Japan is doing—then existing and under-construction LNG facilities will already produce surplus LNG. The first phase of LNG Canada squeaks in, but anything beyond that is highly uncertain, with success premised upon governments backtracking on policy commitments.

Source: IEA

On this basis, the case for public subsidies to tip the scales on the business case and secure new investment is a weak one, fraught with risk to taxpayers.

Turning to the question of climate benefits, as noted above it’s clear that Japan’s interest in Canadian gas isn’t related to emission reductions, but enhancing energy security by replacing Russian gas.

As a result, the prospect of generating legitimate credits under Article 6 seems far-fetched. If both coal and gas demand is falling as nuclear and renewable power increase, how could it be demonstrated that Canadian gas was displacing coal that would otherwise have been burned, rather than replaced with nuclear or renewable power?

Meanwhile, GHG emissions in Canada will increase, either taking us further from achieving our climate targets or requiring other sectors—and citizens—to do more of the heavy lifting.

So things don’t look great, whether considering competitiveness or climate impacts. What business case there is for additional LNG investment in Canada is fraught with uncertainty and risk. If shareholders want to assume that risk, they are free to do so.

But policymakers ought to think twice about public subsidies that put taxpayer money at risk, money that might better support other opportunities that are lower risk and better align with the transition to net zero. As for our climate targets, it’s clear that there is no quid pro quo or net climate benefit resulting from LNG exports. Consequently, governments are well-advised to hold firm on ensuring that any additional LNG development fits within those targets, and the cost of doing so is borne by the industry (not taxpayers or other sectors).

Rachel Samson from the Institute for Research on Public Policy summed things up well, “With many risks facing an LNG project, private investors will focus on the lowest-cost projects with the greatest chance of realizing a return. If government subsidies are added to the mix, projects that are less likely to be competitive – and thus less resilient to shifting market demand – could move forward. If those projects don’t make it, taxpayers are not only short the money invested but they also miss out on the benefits that could have been realized from investing the funds elsewhere.”

Dig down and what seems like a great opportunity may not live up to the hype. All that glitters isn’t gold.